Agentic Commerce: A Love Child of AI and Defi

Exploring the intersection of AI agents and commerce

Putting your Trust in Agents

While not yet widely visible, agents are becoming increasingly pervasive in handling a variety of tasks, ranging from simple prompts to complex multi-step workflows. AI agents have shown early promise to handle knowledge or context-based tasks; everything from design, to code generation, to personal productivity. But they are still plagued with inconsistencies, errors, hallucinations, and often short context windows. In the near-term, humans will still be highly involved to either review, approve, or iterate further with follow-up tasks as agents are beginning to fine-tune their ability to execute these workflows flawlessly.

At a certain point, though, and across different use cases, we will achieve trust in agents to deliver and execute tasks at extremely high confidence levels - we will begin to ask them to do more without our consent or review. However, to do so requires both higher confidence levels and the need to solve for further governance and authorization credentialing.

Today, these interactions look like agents acting on our behalf to engage with a known service, however, tomorrow’s interactions will likely look like an ecosystem of agents acting on our behalf, with unknown/untrusted parties on each side.

A key component of enabling the agent economy will be enabling a commercial transaction. However, today's financial infrastructure and payment rails aren't well-designed in a world of agents and face high points of friction as we seek to have agents handle commerce on our behalf.

Some of the core issues of agents using traditional financial rails include:

- Identity & Authorization: AI agents don't have the same identity markers or behavioral patterns, making it difficult to distinguish between good and bad actors. Agents need to be able to demonstrate proof they are acting on a user's behalf that can be tied back to the original owner.

- Fee Structures & Rigid Barriers: Card processing fees are expensive in the case of microtransactions that are increasingly more common with agent use cases. Larger transactions are likely to face higher friction against traditional fraud checks. Cards are further complicated across borders and delay settlement to minimize risk.

- Programmatic Integration Complexity: Credit cards require complex PCI compliance, tokenization, and fraud prevention measures that add significant overhead to programmatic usage. AI agents need simple, direct payment rails they can use automatically without human intervention for compliance workflows.

- Regulatory and Liability Framework: Credit cards have complex chargeback and dispute resolution processes designed for human based intent, not autonomous agents. This creates unclear liability and dispute resolution paths when agents make payments.

Related, and in addition to the issues highlighted above, there have been several companies taking unique approaches to a potential shift in the agentic economy:

- Shopify recently updated the code of its merchant checkout kit to restrict unauthorized headless checkout agents from transacting on their platform, citing: “Automated scraping, ‘buy-for-me’ agents, or any end-to-end flow that completes payment without a final review step is not permitted”.

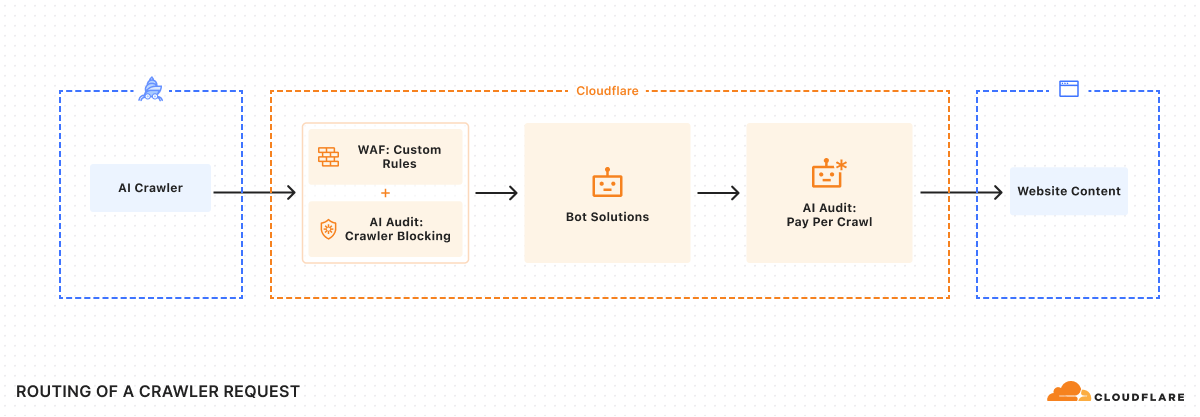

- Cloudflare also recently made headlines, announcing its new Pay-Per-Crawl feature, providing content owners a mechanism to build in programmatic payments to protect against and monetize AI crawler access to web content. If payment is required by the website, crawlers receive a HTTP 402 Payment Required response code, triggering a set of workflows for crawlers to register and submit payment before accessing the requested content.

To enable agent-based commerce, a new set of frameworks, protocols, and payment form factors need to be built or leveraged, with some relevant announcements being made in recent months.

Before getting into frameworks and protocols, the form factor is worth discussing. As referenced above, fiat payments (cards, bank transfer, BNPL, etc) have certain benefits and drawbacks, but will likely face friction until agentic commerce infrastructure is well developed. Stablecoins are becoming another popular option, which are well designed for agentic interactions and are instant, programmable, and flexible across borders. Stablecoins received another victory recently with the passage and signing of the GENIUS Act which sets more clear boundaries for issuers and requirements both domestically and cross-border. This marks an important milestone as we see the B2B economy shift more of their balances into tokenized assets for programmable treasury and automation of AR/AP. But I don’t expect to see a broadscale shift away from fiat payment methods in the near-term, and new payment infrastructure will need to be built to accommodate a wide spectrum of payment types (fiat, stablecoins, and a broader set of cryptocurrencies).

Open Standards & Know Your Agent

In May, Coinbase launched x402 as an open protocol, enabling stablecoin payments via HTTP primarily targeted at agent to service commerce. Similar to Cloudflare’s PPC infrastructure, agents are met with a 402 payment response code and instructions on acceptable tokens, price, etc. While its ecosystem is still in the early stages of being developed, this represents an opportunity for automated microtransactions and accelerated use of stablecoins. Coinbase extends payment capabilities through its facilitator service, which routes payments via its Layer 2 Base network, handling verification and settlement. Relatedly, BitGPT is building additional functionality on the x402 protocol via h402 which expands payment functionality to a broader universe of cryptocurrencies and fiat.

Other standards are also being developed to improve interoperability, identity, and governance (trust/security), increasing the ability to drive broader adoption.

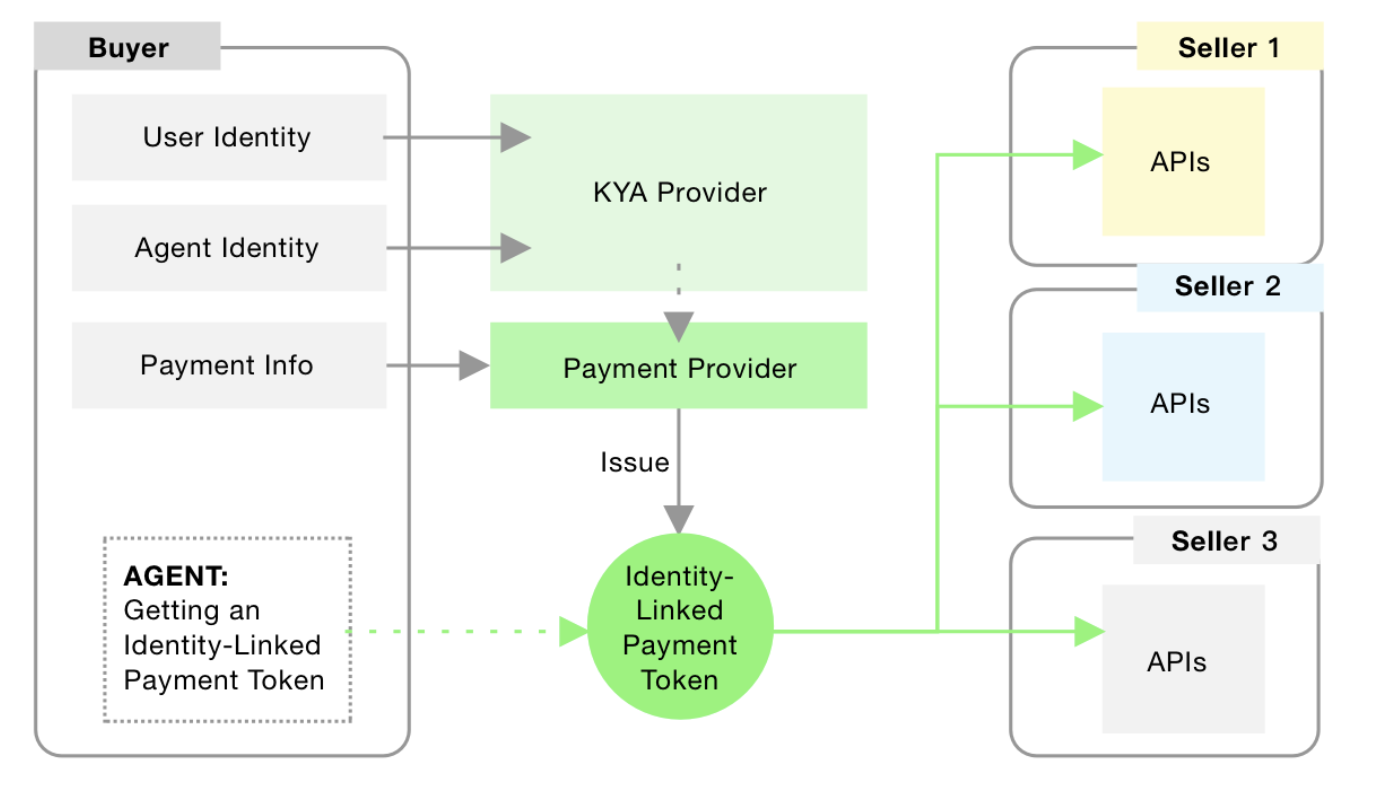

- Founded by a former Circle co-founder, Catena Labs aims to bridge the gap between AI and financial services. To power this vision, they’ve open-sourced the Agent Commerce Kit (ACK) which creates a de-coupled standard for identity (ACK-ID) and payments (ACK-Pay)

- ACK-ID leverages W3C standards to create agent identity tied back to the original owner through the combined use of:

- Decentralized Identifiers (DIDs): a unique cryptographic digital identity that the owner controls.

- Verified Credentials (VCs): tamper-proof digital certificates that contain verified information about the DID holder that can be shared while maintaining privacy.

- ACK-Pay is designed to be transport agnostic, meaning it aims to provide an open, interoperable standard for agents to interact with hosted services and for agent-to-agent transactions across:

- HTTP - Coinbase’s x402 or BitGPT’s h402 protocols

- Google’s Agent to Agent (A2A) or other emerging protocols (i.e. LOKA)

- Major Payment Networks (Mastercard Agent Pay, Visa Intelligent Commerce)

- ACK-ID leverages W3C standards to create agent identity tied back to the original owner through the combined use of:

- Skyfire is another well funded example, founded by former Ripple veterans, similarly electing to open source their identity-linked protocol, KYAPay. KYAPay's architecture leverages JSON Web Tokens to create both identity tokens (KYA - Know Your Agent) and programmable payment tokens, enabling secure transactions across different agent protocols.

- While early, ACK and KYAPay represent potential open standards to solve some of the highlighted gaps in identity and interoperability. Across both open source and commercial offerings, governance and policy management will need to be developed further to ensure agents have proper guardrails as they learn to transact (i.e. payment limits, negotiation, receipts, etc).

- These protocols and commercial offerings will surface additional build out needs to provide further security enhancements, fraud protections, and authorization controls to ensure agentic payments can be used safely.

If you build it, WILL they come?

The infrastructure buildout is underway and drawing a lot of excitement towards agentic commerce, but questions still surround the killer use cases that will drive sizable transaction volume longer term. Some use cases are emerging but are still fairly nascent in terms of adoption. Below are a few examples of current or potential use cases:

- Microtransactions: Pay per crawl, or pay per use of content, API calls, compute, etc.

- Collateral Based Lending: One of the key provisions of the GENIUS Act allows for institutions the ability to post, move, and settle assets in real-time across exchanges, custodians, and DeFi protocols, and use USDC (or other acceptable assets) as collateral for margin.

- Supply Chain Procurement: Autonomous restocking and reordering triggered as stocks fall. Procurement agents can identify alternative suppliers due to timing delays, pricing or tariff impacts, etc

- Consumer Commerce: Perplexity Commerce and Daydream are examples being built and developed further. Large eCommerce players are also developing their own capabilities

- Agentic Bounty Payouts: As Enterprises increase adoption of agents, bounty bug payouts can be automated.

While there are many other use cases and those that have yet to emerge, agent based commerce will play a large role in how the AI economy is built in the years to come. I’m excited to continue to meet many of the builders creating the foundation.

Get in touch